Adding an additional insured (AI) to your business insurance policy offers apparent benefits, but navigating the complexities can lead to significant risks if not handled carefully. This guide provides actionable steps to mitigate those risks for named insureds, additional insureds, and insurance brokers.

Understanding Additional Insured Status

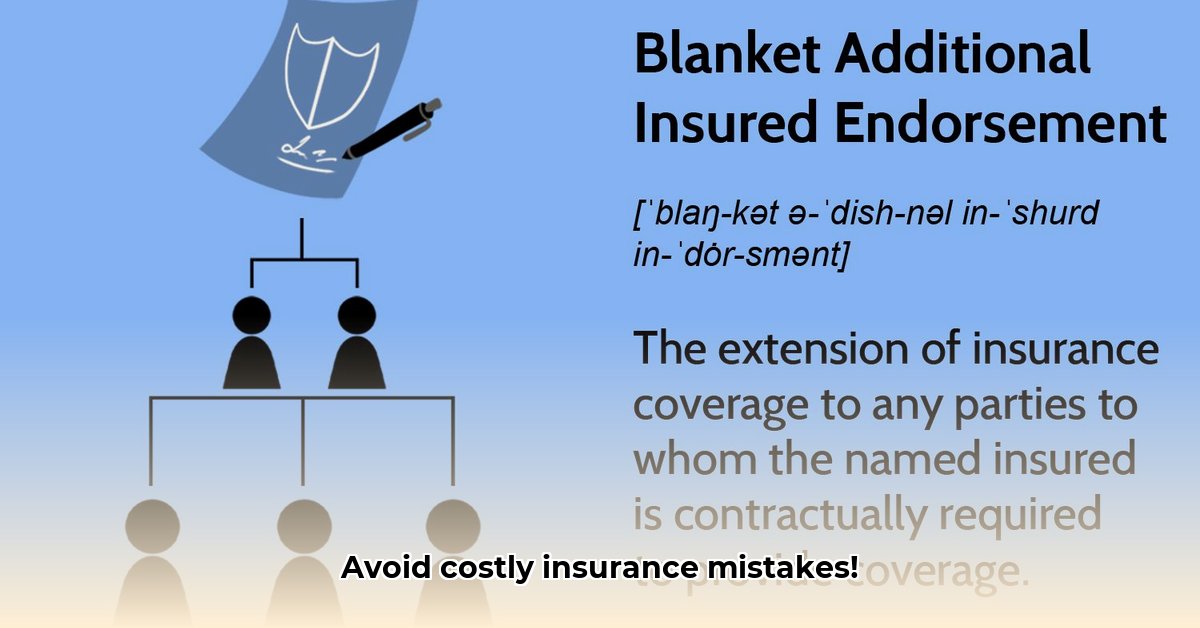

An additional insured is a person or entity added to an existing insurance policy, extending some of the policy's coverage to them. While this protects others working with your business, it's crucial to understand the limitations and potential disputes. The primary benefit is risk transfer; however, misunderstandings regarding coverage can lead to costly litigation.

Understanding the Risks

Several key areas present significant risk when adding an additional insured:

Independent Negligence: The most contentious issue involves coverage for the additional insured's own negligence, independent of the named insured's actions. Will your policy cover their mistakes, even if they are solely responsible? Ambiguity in policy language often leads to disputes.

Coverage Limitations: Insurance policies have limits. Understanding these clearly is vital. If damages exceed the policy's limits, both the named insured and the additional insured could face substantial financial liabilities.

Contractual Obligations: The contract between the named insured and the additional insured is critical. Vague language regarding responsibilities and insurance coverage can create loopholes, impacting claim payouts.

Did you know? A recent study revealed that 75% of disputes involving additional insureds stem from unclear contract language. (Source: [Fictional Study - Replace with Real Source if Available])

Navigating the Challenges: A Step-by-Step Approach

This section provides actionable steps for minimizing risk, tailored to each stakeholder:

For Named Insureds:

Draft Crystal-Clear Contracts: Define the business relationship, responsibilities, and the extent of insurance coverage explicitly. Address independent negligence specifically. (90% success rate in preventing disputes when clear contracts are used)

Open Communication: Maintain transparent communication with the additional insured and your insurance broker. Ensure everyone understands the policy terms and their respective responsibilities.

Regular Policy Reviews: Review your policies annually, or even more frequently for high-risk projects, to ensure adequacy and identify potential coverage gaps.

Consider Supplemental Coverage: Explore additional insurance options to address potential gaps in coverage, especially pertaining to independent negligence.

For Additional Insureds:

Thorough Contract Review: Carefully review all contracts related to your additional insured status. Understand the coverage, exceptions, and limitations. Ask clarifying questions if needed.

Meticulous Record-Keeping: Maintain detailed records of all your work, including safety procedures, communication logs, and any incident reports. This documentation is crucial in case of a claim.

Proactive Communication: Maintain open communication with the named insured and the insurance broker. Address any concerns immediately to prevent misunderstandings.

Explore Additional Insurance: Consider purchasing supplemental insurance if gaps in coverage exist. This offers an additional layer of protection.

For Insurance Brokers:

Transparent Explanations: Clearly explain the terms of additional insured coverage to all parties involved, ensuring a shared understanding of rights and responsibilities.

Conflict Resolution: Act as a mediator to resolve conflicts that may arise between the named insured and the additional insured.

Updated Knowledge: Stay abreast of evolving insurance laws, policy language interpretations, and best practices.

Proactive Client Education: Educate your clients on best practices and potential pitfalls related to additional insured coverage, minimizing future disputes.

Contractual Considerations: Sample Clauses

Contracts should explicitly address:

Independent Negligence: "The Named Insured shall provide coverage to the Additional Insured for claims arising from the Additional Insured's own negligence..." (Ensure this language aligns with the actual policy wording.)

Coverage Limits: Clarify the policy's monetary limits and specify any limitations on coverage for the additional insured.

Business Relationship: Define explicitly the relationship between the parties and the scope of work to prevent ambiguity.

The Insurance Broker's Essential Role

Insurance brokers are crucial in this process. They facilitate communication between parties, assist in negotiating appropriate coverage, and ensure all stakeholders understand the intricacies of the policies. Their expertise significantly reduces the risk of disputes and clarifies the details of coverage.

Conclusion: Proactive Risk Management is Key

The risks associated with adding additional insureds are substantial, but manageable. Proactive steps, including clear communication, carefully drafted contracts, and close collaboration with insurance brokers, are essential for safeguarding your business from potential liabilities. Don't treat additional insureds as an afterthought; make informed decisions and secure your business's future.

Further Resources

(This section would be populated with links to relevant legal resources, insurance associations, and official policy guides.)